By Ty Findley, Co-Founder & General Partner & Colleen Konetzke, Principal

At Ironspring Ventures, we focus on backing innovators in massive industries that make modern life possible, industries that are often out of sight and out of mind to the general public. The distribution of building materials, which we will do our best to roughly define in this research, is one of those industries that is now going through rapid transformation. While we have been deeply involved and investing in this space since our inception, building materials distribution has recently been thrust into the spotlight after three massive market movers announced the following deal activity:

How does a product go from production to inclusion in the built environment? How did that general contractor build that building? What steps were involved? Where did the building materials come from? Who were the key stakeholders and how did they work together to complete these builds? The building materials value chain is the intricate network of players, processes, and activities involved in getting building materials from their raw form to being utilized on the job site. The uniqueness of these processes, coupled with the temporary, project-oriented nature of relationships within the supply chain, leads to a significantly fragmented industry structure. And while we know this is an oversimplification to keep this research easily digestible, the rough value chain looks like this:

Players: Mining companies, quarries, lumber mills, etc.

Activities: Extracting resources, refining them into usable materials, and initial processing

Players: Building material manufacturers, distributors, wholesalers

Activities: Converting processed materials into final building products (e.g., windows, concrete, insulation), packaging, and transporting them to warehouses or distribution centers

Players: Architects, engineers, contractors, subcontractors, purchasing agents

Activities: Identifying project needs, sourcing materials from distributors or manufacturers, negotiating prices and contracts, managing purchase orders

Players: Transportation companies, logistics providers, delivery drivers

Activities: Transporting materials from warehouses or distribution centers to job sites, ensuring safe and timely delivery, managing inventory levels on site

Players: Construction workers, inspectors, quality control specialists

Activities: Verifying quality and quantity of delivered materials, installing materials according to specifications, managing waste and returns

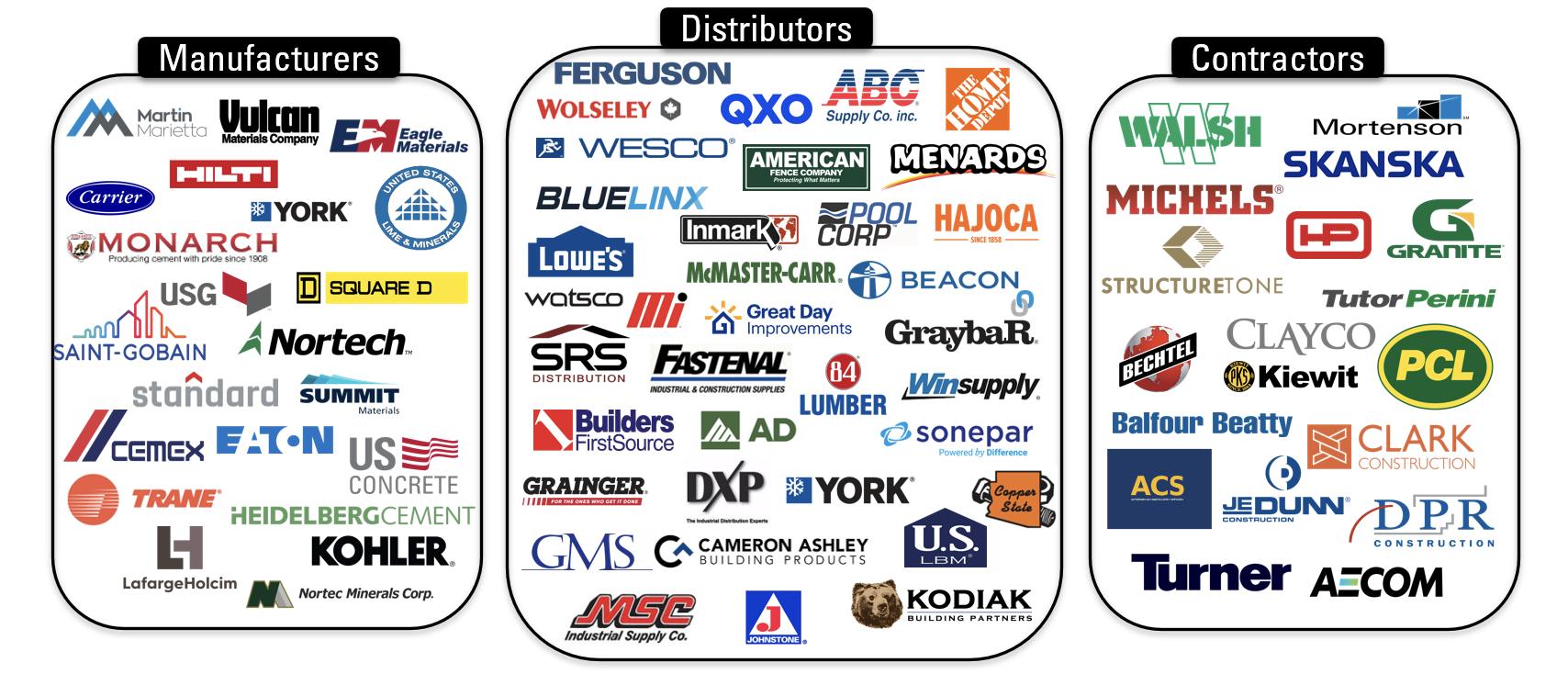

To simplify further, this value chain in its simplest and most common form is manufacturers selling to distributors who sell to contractors. Again, there are plenty of exceptions to our oversimplification, including manufacturers who sell direct or also act as distributors (e.g., Hilti) as one example, but the market generally follows the manufacturer – distributor – contractor flow.

To get a little more detailed as we progress, what do we mean by building materials? Generally it includes, but is not limited to the following: raw materials and aggregates, construction supplies, all things electrical, pre-built components such as doors and windows, fencing and decking, roofing, landscaping, HVAC, pool materials, infrastructure, plumbing, siding, lumber, and water, among so many others we could list out. For the purpose of this piece, and while lines certainly blur in some regards, we refer to the three primary actors in this story as the manufacturer, distributor, and contractor.

Manufacturing is characterized by the significant presence of large, multinational manufacturers (discrete, process, etc.) who offer a diverse array of products and services worldwide. These companies can range from large corporations that produce a wide range of building materials, such as lumber, concrete, and roofing materials, to smaller manufacturers that specialize in specific products like windows, doors, or insulation. On the distribution front, the landscape is notably fragmented, with an estimated ~10,000 distributors in North America and ~25,000 in Europe. Building materials distribution is expected to grow as an industry ~5-9% through 2031. While many in the industry may recognize the large general contractors on the top ENR list each year, the contractor landscape is still similarly fragmented, driven by a majority of highly localized, family-run businesses. As a salient example of the challenge distributors face serving contractor fragmentation, SRS outlines it serves over 130,000 different contractor customers themselves alone, with only one customer accounting for more than 1% of their total sales!

Across the board, manufacturers, distributors, and contractors are increasingly incorporating technology into their operations, spurred by technological advancement in other industries as well as construction’s ever changing needs to eliminate both labor and productivity challenges that arise from such fragmented and offline stakeholders. This “DistributionTech” technological shift is indicative of the sector’s adaptation to the modern construction landscape, pursuing efficiency and sustainability in response to global trends. All of this leads us to the next section at the heart of this research, the “Massive Middle” transformation going on within the distribution industry. While not exhaustive, see who some of the major players are below.

In its simplest form, the building materials distribution value chain runs manufacturer > distributor > contractor. There are of course exceptions, such as direct sales or players operating in more than one section of the value chain, but the majority holds in these three buckets. Many of these players are global but the ones listed below have North America as their primary place of business.

The distributor is responsible for getting the product out to market and into the hands of the customers. Distributors connect suppliers with project sites and contractors, keep stock of a complex array of components and materials, handle logistics, and often provide credit to their customers. Their businesses are built heavily on relationships and trust given the fragmented nature of the markets they operate in. But, for as fragmented and localized as distribution can be, the building materials segment alone is a massive market: $800B across North America and Europe. As noted above, there’s a reason serial billion-dollar-outcome entrepreneur Brad Jacobs is turning his eyes to building products distribution for his next act at QXO, looking to create a digitally-enabled market leader in the space. Also, based here in our home state of Texas, SRS Distribution is a PE-backed platform (Berkshire Partners and Leonard Green & Partners) that has been quietly acquiring smaller distributors and opened a record 22 greenfield locations last year. It’s one of the largest 50 private companies in the US. In March, Home Depot announced a bid to acquire SRS Distribution for $18.25B. This gives Home Depot, which primarily serves weekend DIYers and the small, last-minute needs of contractors, much greater access to contractors directly as well as last mile capabilities that they don’t currently have. SRS has also invested heavily in logistics capabilities, owning and operating a fleet of 4,000 trucks for delivering materials to jobsites. We call the logistics comment out as a key distributor trend we’re seeing accelerate aligned to examples such as Ferguson and Advanced Auto Parts both building out new warehouses across the US to localize product closer to B2B customers who are now expecting the same rapid delivery experience they experience as B2C customers in their personal lives (thank you Amazon). The SRS acquisition was completed this month.

Zooming in a bit on the day- to-day operations, distributors rely primarily on counter sales (in-person) or inside sales. When purchasing millions of dollars’ worth of a specific material that may, for example, support the weight of a building or provide it with electricity, a contractor would rather sit across the table from an expert to ensure they’re buying specifically what they need, rather than order it online or pick it up from a generic retailer. For a smaller order, picture this: a contractor walks into a distributor’s store and has a notepad or a piece of cardboard with what they need to get written on it. Upon returning to the construction site, they realize they didn’t get everything they need. Their team might call the store back or they may make an additional round trip. If they try to call, the phone line may be busy. As we’ll outline below, it’s an understatement to say there’s plenty of opportunities for digitization and automation within this “Massive Middle” ecosystem, but we’re also subject matters experts who appreciate that the expertise and human-level trust of the distributor are of critical importance and will never be automated away.

As mentioned earlier, Ironspring Ventures has been investing heavily in support of advancing this “Massive Middle” since our inception. Below we’ll share more about that and our outlook on the opportunities ahead for what we see as a tidal wave of DistributionTech forming.

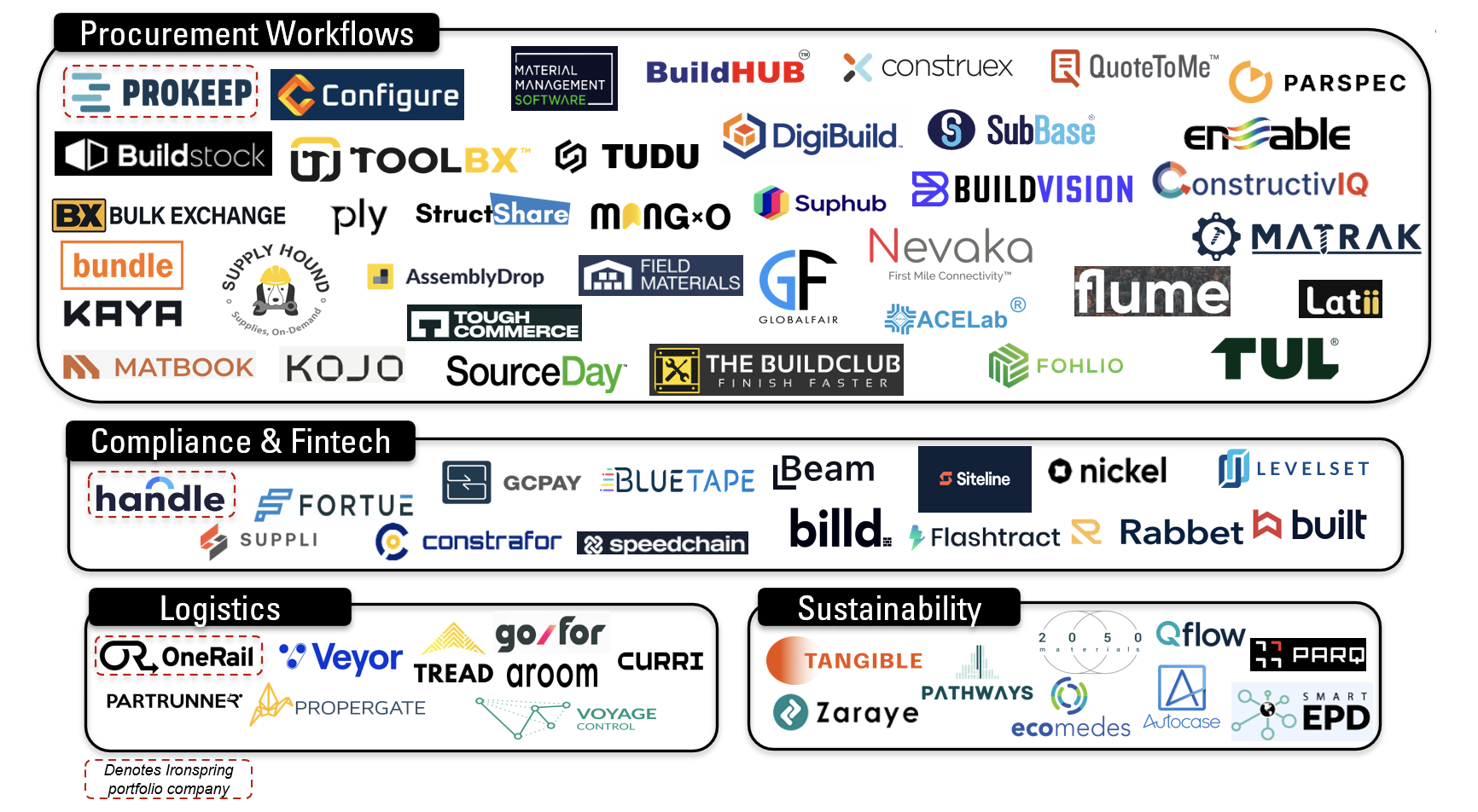

The experience of ordering building materials is far from the experience of ordering your favorite product on Amazon Prime. The value chain is rife with challenges – or as we see them, opportunities – for digital innovation to drive efficiency, transparency, and sustainability for what supplies the growth of our built environment. We see great opportunity for digital innovation across all aspects of the value chain, but below are four areas we believe have immediate innovation potential.

Distribution is estimated to have 7,000+ independent operators in the US, many with just one or two branches. This creates a competitive landscape with diverse offerings and localized expertise. According to the Associated General Contractors of America (AGC), there are over 900,000+ construction businesses in the US. Per Census data, the average establishment has fewer than 10 employees. Companies with 100 or fewer employees retain greater than half of the construction industry’s revenue, with that ratio going to two-thirds within specialty trade contractors specifically. Enterprises typically hold only 10-20% of the market depending on the specialty. Because of this, the purchase of building materials is highly relationship-based. Additionally, about a third of all building materials used in the US every year are imported, adding an additional layer of complexity. Given the fragmented, localized nature of the market, visibility into both supply and demand is opaque. Upstream, manufacturers have little visibility into their ultimate end customers (e.g., contractors, developers, architects, do-it-yourselfers) and interact primarily through wholesalers and retailers. All of which lends to highly complex and inefficient inventory planning and management within these supply chains.

The industry has seen some consolidation as of late. Well-capitalized players are actively acquiring smaller ones, creating super-regional and national players with larger footprints. Examples include Brad Jacobs’ QXO, the now complete SRS Distribution/Home Depot tie-up, and AD and IMARK merging, mentioned above. Increased investment from private equity firms is fueling further consolidation. While consolidation is occurring, it’s unlikely to eliminate the fragmented nature entirely. The vast number of players and diverse subsectors suggest the market will remain complex and competitive for the foreseeable future.

As highlighted in the example above, most customers call to place orders, which is inefficient and time-consuming. Customers on hold hang up out of frustration and when they do get through to a distributor’s desk, the order may not be taken down accurately (the iconic yellow sticky notes…). Increasingly, end consumers are willing to purchase building materials through the internet and mobile apps, just as they do for any other household products, but still very little of the ordering process is digital. Revenue derived from B2B e-commerce is currently only mid-single digits (all of US retail e-commerce penetration is still below 20%), and this share is expected to triple by 2030. For now, placing orders is time-intensive and inefficient, often involving calling multiple distributors and waiting on hold. Additionally, data is not cohesive across the value chain, and its analog nature prevents alignment between players. Manufacturers, distributors, and contractors may refer to a certain product or part as something different. Home Depot brings its digital sales capability to SRS’s network in the recently announced merger mentioned above: Home Depot already has digitized the retail experience for B2C consumers and hopes to leverage that platform to do so for larger, B2B commercial contractors. Ironspring Ventures is a proud investor in Prokeep, a communication and commerce platform specifically built for the internal workflows of distributors, which is bringing more workforce efficiency, higher levels of customer service, and increased top-line revenue potential to combat this purchasing friction.

Contractors must order and pay for materials and products before work is completed and they can receive payment for their work. Delayed payments were estimated to cost the construction industry $136B in 2021. Additionally, the construction lien filing and management process is highly manual. Construction liens are powerful tools for contractors and suppliers to secure payment for their work but also require careful adherence to legal processes and deadlines, and detailed documentation is required. The need for solutions here has been clearly highlighted through the recent capital markets acquisition activity: in Q4’21 Procore (NYSE: PCOR) bought Levelset for $500M, in Q1’24 Autodesk (Nasdaq: ADSK) acquired Payapps, and in Q2’24 Trimble (Nasdaq: TRMB) acquired Flashtract. Ironspring Ventures is a proud investor in Handle, a purpose-built lien management, waiver exchange, and online payments platform for material suppliers, which enables credit and finance teams to better manage cash flows.

Given materials are often bulky, heavy, and oddly-shaped, and not to mention expensive, coordinating their transport and delivery is not as simple as ordering a package on Amazon. Managing product delivery to locations that frequently are remote or lack space to store bulky materials can be a challenge. Managing inventory across the distributor’s network and moving the materials between distributor locations is no small feat. The materials also must be tracked and managed once they are at the construction site. It becomes even clearer why Home Depot acquired SRS: with SRS’s 750+ branches, Home Depot just added over 750 spokes to get materials directly to the job-site. Over the next decade, it’s apparent to us that distribution incumbents who view ‘transportation & logistics’ as not core to their business (i.e., “leave that to the freight experts”) will find themselves falling behind their competitors who are advancing logistics oversight and capabilities internally. Ironspring Ventures is a proud investor in OneRail, an omnichannel fulfillment and last-mile logistics platform with a network of over 12M drivers to complete deliveries, which is providing F100 distributor clients greater operational control over their previously siloed fulfillment and logistics operations.

As we’ve seen, there’s ample opportunity for investment in solutions that change how businesses design, build, distribute, and operate along the building materials value chain. We’ve broken solutions into what problem they are solving, their wedge of value, and how they’re entering the market. Most startups building along the building materials value chain are building for contractors or distributors, with an eye to expand their reach up the value chain to distributors or manufacturers. Each company enters the value chain at a different point – solving one pain point – with many building platforms to solve more than one pain point. And as always with market maps, there are blurred lines between many solution providers and what categories they ultimately touch. We chose simplification over complexity to ensure the primary point is made of just how many innovation entrants are approaching the “Massive Middle” vs the nuanced semantics of categorization.

At Ironspring Ventures, we see distributors and the “Massive Middle” becoming more important than ever in a complex and changing environment for the production, distribution, and use of building materials. Despite some consolidation within distribution, the market remains highly fragmented, as does manufacturing and contracting. Distribution is a relationship business. Those who embrace DistributionTech and adopt digital solutions that can help distributors collect data on, nurture and grow their relationships with upstream and downstream value chain constituents are more likely to be successful.

Additionally, for any new solution to be meaningfully adopted, you need buy-in across the value chain – if distributors want to adopt a new technology, manufacturers and contractors will eventually need to get on board for the tech to really scale. We look for solutions that work within the current systems and ways of working that manufacturers, distributors, and contractors already use. Tools that don’t require a big behavior change and fit in with existing workflows will have more success. If you are building DistributionTech, a corporate with interest in innovating faster, or just generally curious to chat more and help us build ecosystem in support of the rise of building material distributors, please reach out!