By Colleen Konetzke, Principal

Welcome to our third edition of The Blueprint, Ironspring Ventures’ new series to share what we’re thinking about, observing, and predicting across the digital industrial innovation ecosystem. Want to learn more about The Blueprint? Check out this primer as well as our previous pieces on the power of vertical industrial labor solutions and the opportunity nearshoring presents for supply chain innovators in LATAM markets. This edition focuses on why investment in digital industrial innovation is an investment in our planet.

">Let us know what you think – we’re eager to discuss and collaborate.

Investment in industrial tech is an investment in our planet. “Heavy industry” is not thought of as being in the same sentence with “sustainability,” but these often-hidden industries will be at the center of any real transformation to living within our planet’s means while still driving economic growth. At Ironspring Ventures, we look at how things are designed, built, distributed, and operated and back founders and teams that do these in a more productive, sustainable, and secure manner. We lead and co-lead early-stage investments in what we define as digital industrial innovation: startups across construction, manufacturing, transport & logistics, and alternative energy.

Seldom do we stop and ask, “How was that product I bought at the store manufactured? Then delivered? How was that office building constructed? Where does the electricity in my home come from?” These industries we may not see or think about drive our economy in a big way – and have a big footprint that provides ample investment opportunity. It’s not complicated: if you manufacture products closer to demand or with new advanced methods, you can transform their resource use; if you change how you construct buildings, you can slash material waste; if you move goods around more optimally, you can cut tons of CO2 emissions, and if you change how all of this is powered, you can reduce planetary impact – to give just a few examples of investment opportunities. Let’s look at each of our four core sectors in turn and understand their current size and impact.

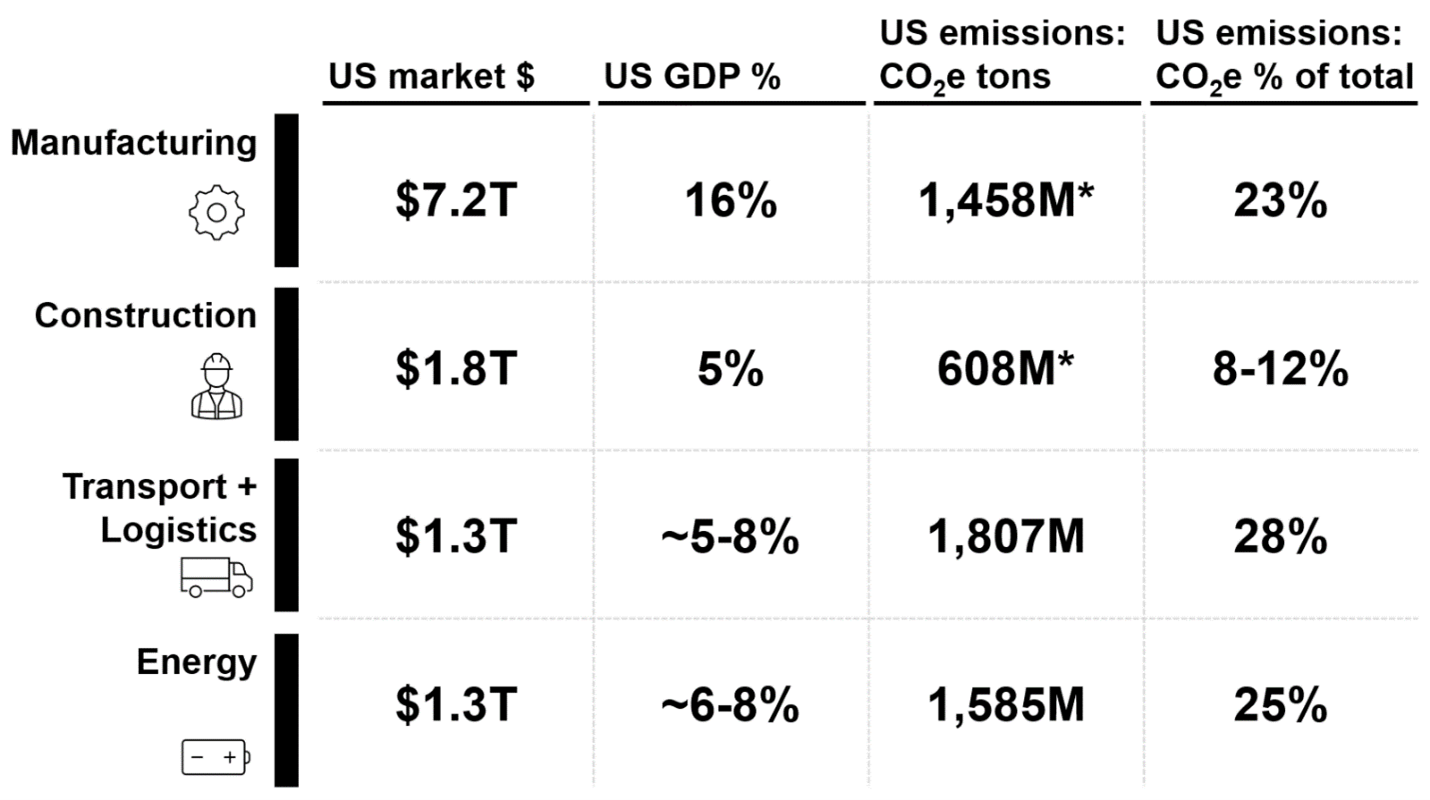

Manufacturing, construction, transport and logistics, and energy are the building blocks of modern society. Below is an appreciation of the size of each of these areas to understand why even small changes can make a major difference.

We aren’t going to stop building, making, or moving things, but there is an enormous opportunity to change and invest in how we go about it. These sectors that are the building blocks of a functional society are largely reliant upon systems, tools, and business models that are dated and inefficient. Below we scratch the surface of the opportunity within each.

Manufacturing is having a moment: We are in the middle of an American manufacturing renaissance. Since the late ‘90s, the US has lost a quarter of all manufacturing firms and 4.5M manufacturing jobs. The pandemic, conflict, and escalating geopolitical tensions between major global powers highlighted that hindsight is always 20-20; it was cheaper to produce goods somewhere else in the past, but the US now lacks manufacturing capacity and know-how for critical goods like medical supplies, microchips, solar panels, and batteries. Sourcing goods like these from outside the US has become a concern of economic security and energy independence. For example: in 2022, 77% of EV battery production capacity was based in China. Taiwan produces over 60% of the world’s semiconductors. The solar supply chain – from raw materials to finished panels – is also controlled primarily by China, which owns and controls 75% of production capacity (or more) for each major piece of the solar supply chain.

Where there’s risk and imbalance, there also lies major opportunity. These concerns have spurred legislation such as the CHIPS Act, the Infrastructure Investment and Jobs Act (IIJA), and the Inflation Reduction Act (IRA), all of which provided direct funding and tax incentives for public and private manufacturing facilities. These in turn have spurred massive manufacturing investment in the US – requiring massive construction efforts, as covered below, and adding approximately 250,000 jobs over the next two years. While these investments may not bear fruit in the short term because it takes time to build factories and get them up and running, they promise a more energy independent future and a more stable and sustainable supply chain less exposed to geopolitical conflict.

According to McKinsey, an effective digital transformation of the US manufacturing sector could boost US GDP by $275B and add up to 1.5M jobs. Digitally enabled manufacturing offers new opportunities for businesses to optimize production for sustainability. Examples of digital applications include: IIoT (industrial internet of things) use in factories to minimize errors and leveraging digital inventory that allows for parts to be produced on-demand to minimize waste. Finally, new techniques like additive manufacturing use less material, produce less waste, and can be faster and more cost efficient. Ironspring is keen to learn about companies innovating in these areas, as well as others connecting the disparate manufacturing tech stack.

While investment in the construction industry has stayed relatively consistent, productivity has declined on a per worker basis and productivity of the industry overall has only improved by about 1%. Construction remains one of the least digitized industries and is incredibly risk averse. Because each project is a unique challenge, construction doesn’t enjoy the economies of scale seen in other industries. Construction is also heavily reliant on manual labor and processes, and there’s a historic shortage of that labor, north of 500,000 jobs.

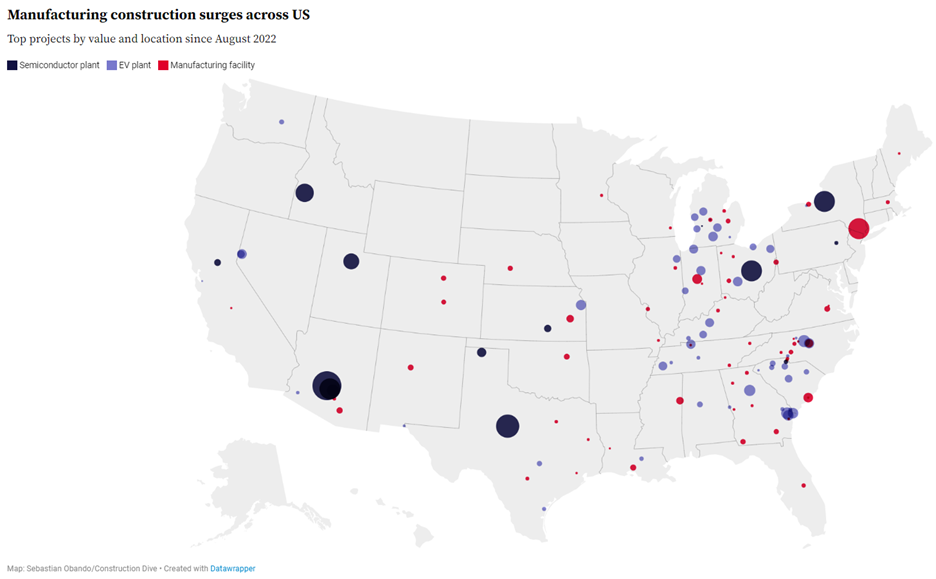

All of the required infrastructure for a transition to a more sustainable economy – power plants, wind farms, solar farms, battery factories, you name it – must be built, and fast. A tremendous amount of capital has been committed and will continue to pour into large energy and infrastructure projects in the US. The bipartisan IIJA will inject $1.2T into the nation’s infrastructure. And of course, lest we forget the current manufacturing megaproject melee pictured above, the CHIPS Act and IRA are contributing to a manufacturing boom. The renewed push to revive American manufacturing after decades of offshoring has led to over $516B in private company investment so far. Through August of 2023, manufacturing construction spending increased 65.5% in 12 months.

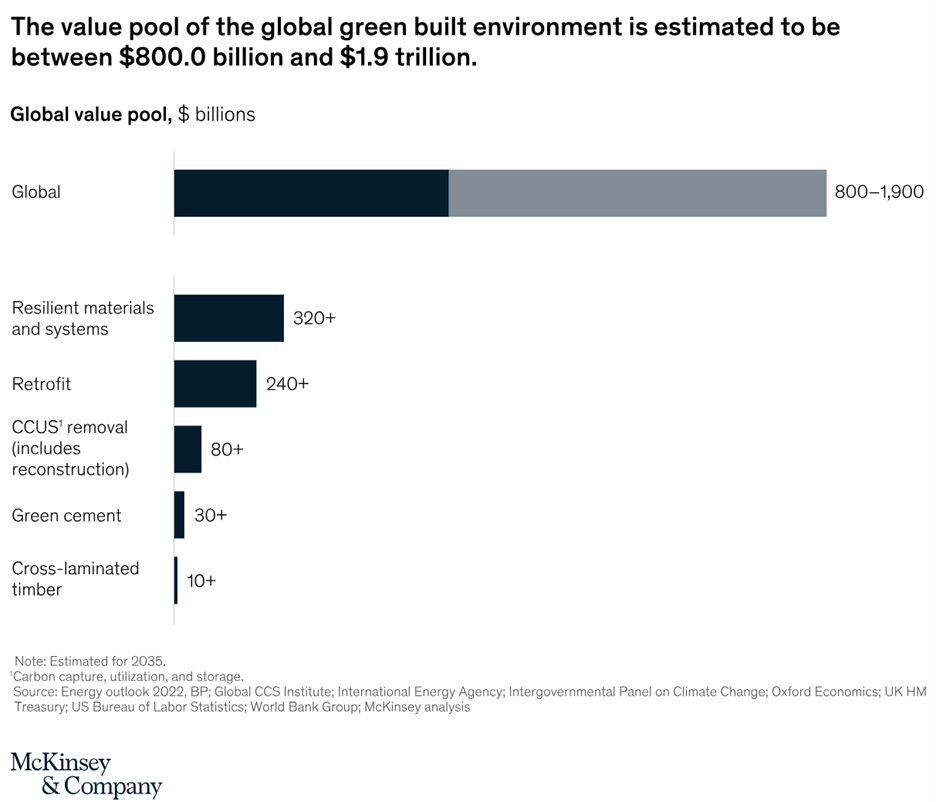

For construction to step up to the plate, investment and innovation are direly needed. The transformation of construction provides ample opportunity: decarbonizing the built environment can create as much as $800B to $1.9T in new green value pools across sectors according to a recent McKinsey study (below).

Digital solutions can avoid rework, require fewer laborers, and speed up the construction process. We are excited about new building methods – 3D printing and modular building, to name a few – that change the way buildings are constructed. Other digital solutions like marketplaces or documentation tools expedite the production and movement of newer, greener materials and reduce the soft costs associated with producing and selling these materials.

Business risk, new consumer habits, and changing regulations have all shone a spotlight on how goods move. The Covid-19 pandemic and ensuing supply chain snarls showed just how fragile pre-pandemic global supply chains were. In 2020, e-commerce sales in the US more than doubled from the previous year to 35%, thanks to the pandemic. Recent legislation – the IRA, as well as federal requirements to procure goods that are sustainable and American made – has put a price tag on understanding where something was manufactured, assembled, and moved in order to unlock incentives and demand. Finally, scope 3 emissions, the CO2 emissions associated with supply chains upstream and downstream of a business, are gaining more attention. RMI reports that the average company’s supply chain greenhouse gas emissions are 5.5 times higher than the direct emissions from its own assets and operations. While the SEC has moved away from requiring scope 3 reporting in the near term, it is anticipated that it will eventually be required, and California has already moved to require such reporting. That means that reporting businesses will need to have a detailed understanding of how their supply chains function.

Despite the increased attention on transport and logistics, key challenges remain, especially around labor and efficiency. There is a persistent truck driver shortage in the US – or rather, an economic shortage of opportunity, pushing drivers out of the market – plaguing the industry with labor woes. The US has recently been shifting trading partners relatively quickly, with Mexico stepping into the spotlight. Questions remain about its ability to step up into the role because of infrastructure, water, and electricity constraints, among other challenges. The trucking industry, still reliant on analog systems, also has a waste problem; the Bureau of Transportation Statistics estimates 87M tons of emissions from trucking come from empty non-revenue miles.

We see numerous opportunities within transport and logistics: maximizing efficiency, increasing visibility, and changing what powers transport. A whopping 35% percent of trucks on the road today are traveling empty. Eliminating empty miles to get better rates reduces carbon emissions. Visibility applications lay the groundwork for emissions tracking. Finally, much of transportation is moving towards electric engines, which are significantly more energy efficient. EVs are ~3x more effective at converting energy into motion than ICEVs (internal combustion vehicles), with an average efficiency of 60-70%, compared to 20-30% for ICEVs. In many instances within transportation, the same investments that reduce spend also reduce emissions.

The way we produce, move, and use energy in the US is changing. The antiquated electric grid we currently operate on was designed for combustion-fueled power to move often long distances from large, centralized power plants in one direction to the end use consumer. Of all the electricity produced by the power sector in the US, 35% reaches end users, while 65% falls to electrical system energy losses primarily from steam-electric and combustion turbines. The introduction of renewable, distributed energy is turning our current grid on its head and introducing new challenges. The electrification of processes formerly powered by fossil fuels, transportation in particular, is expected to increase electricity demand 50-100% over the coming decades. Demand has stagnated in recent years, deviating from economic growth thanks to electrical efficiency gains, so infrastructure has not kept pace with forthcoming demand expected from large-scale electrification.

As the lifeblood of the economy, energy cuts across the heavy industries in our focus – these industries rely heavily on energy, and in turn these industries will help transform energy. Manufacturing, construction, and transport and logistics will drive the energy transition and make it physically happen. Industrial energy use accounts for 33% of US electricity use, and manufacturing claims 76% of that. The growth of renewable energy is already driving massive construction of infrastructure and manufacturing, as demonstrated above. $372B in utility-scale clean energy projects has been announced in the 15 months since the IRA passed – the same amount as the previous decade, but construction productivity hasn’t kept pace to build these projects 10 times as fast. Hardware, planning, and installation for public EV charging could cost $35B+ through 2030. Finally, producing power closer to where it will be used can help eliminate losses from transporting power. That coupled with demand response helps manage peaks and valleys in power demanded, cutting infrastructure investment needs.

Sustainability rhetoric has typically been around tradeoffs: growth at the expense of sustainability, or sustainability at the expense of profits. We invest so that these industries can design, build, distribute, and operate and have less of an impact on the environment. When it comes to the dollars flowing in, we see a huge gap in investment between other sectors and heavy industry, with fewer dollars flowing into heavy industry proportional to its economic and environmental impact. We are looking for digital tools and novel business models transforming our focus sectors. We often ask ourselves: does the technology help our industries save time, save energy, or save materials, and if so, how does that translate into a clear economic return on investment? Ultimately, saving any of these resources can be translated to both reduced CO2 emission equivalents and money saved, incentivizing all stakeholders on all sides of the table. Accounting for greenhouse gases accurately will be critical – you cannot manage what you don’t measure – but legacy industry currently often lacks the data and capability to accurately do so given its use of old, analog systems. We continue to look for companies that can drive accountability and clarity in heavy industry.

Through our deep network, Ironspring Ventures is uniquely positioned to make a big impact in these sectors – and we already are. In our portfolio today:

There’s ample opportunity to invest in industrial transformation. Does your company take an analog process and make it digital? Does it save heavy industry time, energy, or materials? Does it allow legacy industry to design, build, distribute, or operate in a new way? Reach out to us, we’d love to hear from you.